Salesforce’s trajectory - from a non-existent startup in 1999 to the undisputed market leader by 2012 - remains one of the most successful execution plays in enterprise software history. As of 2026, Salesforce continues to anchor the CRM category, yet its sustained dominance is as much a result of strategic positioning as it is technical innovation.

Source: Gartner SFA MQ evolution - a visual representation of sustained market leadership.

Source: Gartner SFA MQ evolution - a visual representation of sustained market leadership.

Success in the technology sector is rarely permanent. To understand how Salesforce captured the market and - more importantly - how it must defend it, I recently revisited the late Clayton Christensen’s foundational work on Disruptive Innovation. Christensen, the father of disruption theory and author of The Innovator’s Dilemma, provided a framework that perfectly distils the Salesforce journey.

As a market analyst looking at the 2026 landscape, we must ask: how does Christensen’s theory apply to a dominant incumbent that is now frequently the target of the very disruption it once pioneered?

The Cloud Genesis: A Textbook Disruptor

Founded in 1999, Salesforce was the quintessential disruptive technology. Marc Benioff’s vision was to make enterprise software “as easy as buying a book on Amazon” - a radical proposition in an era of heavy, on-premise deployments.

The disruption wasn’t just technical; it was structural. While incumbents like Oracle and SAP were locked into high - margin, upfront licensing models with heavy professional service requirements, Salesforce introduced a subscription - based profit model. By abstracting away host infrastructure and operational support, they lowered the barrier to entry for CRM adoption to near zero.

This shift prioritised “customer success” and adoption over the “big bang” sale. In the cloud model, if a customer doesn’t find value, they stop paying. This fundamental alignment of incentives propelled Salesforce past legacy giants whose business models relied on “shelfware” - software bought but never used.

New Market Disruption: Capturing the Footrest

According to Christensen’s theory, “New Market Disruption” occurs when an innovation targets “non - consumption” - consumers who historically lacked the money or skill to use the existing products in the market.

In 1999, many small - to - medium businesses (SMBs) didn’t have a CRM. They used spreadsheets, Access databases, or physical ledgers because the enterprise incumbents were too expensive and complex.

By entering the market with a low - cost, accessible subscription, Salesforce didn’t need to match the feature depth of Siebel or Oracle on day one. They simply needed to be “good enough” for the bottom end of the market. However, by constantly iterating - famously delivering three major releases per year - they quickly bridged the performance gap and moved up - market.

The ‘Job to be Done’ (JTBD)

A central pillar of Christensen’s strategy is the “Jobs to be Done” theory. Most companies fail because they focus on products and attributes rather than why a customer “hires” them.

Salesforce has historically understood its “job” better than anyone: helping companies connect with their customers. The Salesforce platform wasn’t “hired” to be a database; it was hired to provide a “360 - degree view” of the customer so that sales, service, and marketing teams could act with precision.

Source: Dreamforce represents the physical manifestations of the Salesforce ecosystem and community.

Source: Dreamforce represents the physical manifestations of the Salesforce ecosystem and community.

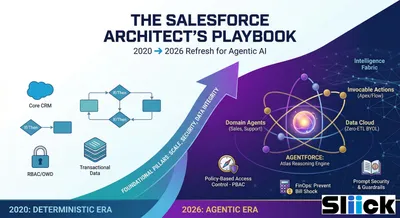

In 1999, that “job” was basic contact management. In 2026, that job has evolved into agentic customer engagement. With the heavy push into Agentforce, the “job” is now about synthesising massive data volumes into autonomous actions. The return on investment (ROI) is no longer just about process efficiency - it is about business outcomes driven by agentic workforces.

The Analyst View: Maintaining the Disruptive Edge

As Salesforce matures into a titan with a market cap exceeding $300 billion, it faces the classic “Innovator’s Dilemma.” How does a company that has moved so far up - market continue to innovate without being disrupted from below?

1. Countering the Low - End Disruptors

Just as Salesforce once “fled” the low - margin SMB market to chase enterprise whales, new entrants are now targeting the bottom end of the market with hyper - verticalised, AI - native solutions. Using modern, nimble technology stacks, these disruptors fly under the radar of enterprise procurement until they have matured enough to compete at the top. Salesforce must ensure its “Starter” and “Pro” suites remain competitive, or it risks losing the next generation of enterprise leaders at the seed stage.

2. The Challenge of Self - Disruption

Christensen argued that a company cannot easily disrupt itself because its existing profit model and KPIs act as a gravitational pull toward “sustaining innovations” (making existing products better for existing customers).

To counter this, Salesforce has historically used strategic acquisitions - such as MuleSoft, Tableau, Slack, and now the heavy push into Agentforce - to pivot its core. In the agentic era, Salesforce must be willing to cannibalise its traditional “seat - based” licensing if “outcome - based” or “consumption - based” models are what the market demands.

3. Modularisation vs. Integration

Disruption theory predicts that as a market matures, modular architectures eventually defeat integrated ones. Highly specialised companies will often outperform a generalist “all - in - one” suite if they can be easily swapped in and out.

Salesforce’s current strategy is one of deep integration (the “Core” platform). However, to remain the “Operating System for Business,” it must maintain its commitment to an open ecosystem. Agentforce acts as the modern modular layer - allowing Salesforce to “deploy” intelligence across any system without requiring the customer to move everything into the CRM.

4. Radical Simplicity in a Complex World

The Salesforce platform has grown exponentially since 1999. With hundreds of products and thousands of features, it is no longer “as easy as buying a book on Amazon.”

The greatest threat to Salesforce isn’t a lack of features; it is “cognitive overhead.” As an architect, my recommendation is a return to radical simplicity. The “Job to be Done” for 2026 is helping customers cut through the noise. Features like “Automated Health Checks” and “Agent Builder” are steps in the right direction, but the platform must continue to hide its complexity behind intelligent, autonomous interfaces.

Salesforce achieved its success by being the disruptor. Now, as the bedrock of the enterprise software stack, it must navigate the most significant shift since the cloud: the move from “Software as a Service” to “Intelligence as a Service.”

By staying aligned with the “Job to be Done” and remaining vigilant against low - end disruption, Salesforce can ensure that its next 27 years are as impactful as its first. Success is never permanent - it must be re-earned through every architectural decision and every customer interaction.

Disclaimer: This analysis reflects the author’s interpretation of Disruptive Strategy and does not represent internal Salesforce strategy.